Updated at 10/06/2022 - 09:27 am

Over the past 30 years of renewing and attracting foreign direct investment, Vietnam has made strong strides in economic development. Foreign direct investment from multinational companies (MNCs) is the solution to the problem of how to improve economic management, attract innovation in technology application and create jobs for people. labor. However, other shortcomings that need to be managed such as tax loss, even no tax collection from these MNCs are always concerned and managed by governments based on OECD recommendations. . Therefore, the identification of transfer pricing methods to effectively control transfer pricing is a top priority issue through the combination and joint implementation of countries around the world.

Slippage of loss or volatility reduces profits or causes losses #

Transfer pricing through buying and selling raw materials, semi-finished products or goods with parent company or affiliated company

This transfer pricing is done through high tax rate country-based multinational corporations buying raw materials, semi-finished products or finished products at high prices and then reselling them. for other member companies at low prices to minimize profits, thereby minimizing tax payable, even causing "fake loss, real profit", not having to fulfill obligations tax. In many cases, enterprises do not directly deal with the parent company, but deal with the affiliated parties of the parent company. In these cases, the state management agencies, and in many cases, the joint venture parties are not even aware of it.

In a similar way to the valuation of fixed assets mentioned above, firms that are partners in special relationships can also negotiate prices of raw materials for each other in the direction of higher declarations. at market price.

This is also one of the ways for companies to remit profits abroad through paying for imported goods with the parent company or another branch in MNCs. FDI enterprises' import of raw materials from abroad is also one of the factors leading to the fact that the recipient countries have a balance of payments tilted towards trade deficit.

Transfer pricing through capital contribution enhancement

This is one of the typical forms of price transfer when MNCs carry out foreign investment in the form of a joint venture or establish a company with 100% foreign capital.

When investing in the form of a joint venture, in the first stage, price transfer is done step by step through capital contribution: foreign investors invest through capital contribution to enterprises by machinery, equipment and technology. . The majority of domestic enterprises have limited financial resources, so they contribute capital mainly with land use rights. However, land use value is often underestimated, while machinery and equipment contributed by foreign investors are often unique, out of date or fully amortized, but by domestic enterprises. limited appraisal capacity and qualifications, lack of information and databases for comparison, so in the pricing process, these machines, equipment and technologies are often pushed much higher than their prices. its real value.

In the form of investment to establish a company with 100% foreign capital, the increase in the value of assets contributed as capital will help the investor increase the annual depreciation rate, ie increase input costs. This will help the investor to quickly return the fixed investment, thereby reducing investment risks, and also reducing the CIT obligation to be paid in the host country.

Transfer prices by short raising the value of intangible assets, buying and selling fixed assets at high prices

Another popular form of capital contribution by foreign investors is capital contribution with intangible assets: technology software, brands, recipes ... that the valuation of these assets is often It is also very difficult, since there are no specific standards for evaluation. Foreign investors' short increase in the value of intangible assets in the capital contribution process will help increase the capital contribution ratio of foreign investors, thereby determining the voice in the business.

In addition to capital contribution with intangible assets, foreign investors also transfer production and business technology to associated parties in the host country and collect royalties. Under current regulations in most countries, royalties are subject to a much lower tax rate than corporate income tax rates (most set rates for royalties at 5 %; 7,5%; 10%; 15%). Thus, foreign investors have saved a lot of net profits when converting forms from paying royalties instead of dividends.

In the trade of tangible fixed assets, multinational corporation companies headquartered in countries with high tax rates will buy tangible fixed assets of companies with headquarters. low tax rates for very high prices relative to the real value of the property. Through the purchase and sale of these fixed assets, part of the company's income is transferred abroad to another company in the same group. Therefore, the company's profits decrease thereby reducing the amount of tax payable.

Similar to buying and selling tangible fixed assets, companies will value intangible fixed assets very high or pay for the costs of branding, product development, advertising, marketing ... at member companies based in a country with a high corporate income tax rate. If the costs incurred will be borne by the firms with the high tax rate, the benefits are equal to all member companies. It also minimizes the amount of tax payable and helps multinationals save the cost of liquidating obsolete fixed assets.

Transfer pricing by increasing administrative and administrative costs

One of the positive effects of foreign direct investment inflows on receiving countries, especially developing countries, is gaining advanced management experience. However, on the other hand, it is undeniable that this is also one of the common forms that companies carry out to remit profits under different names:

- The MNCs branch undertakes to hire a manager with a high salary, and at the same time pay a sum of money to the foreign parent company or another branch for providing the manager.

- Enterprises send experts and workers to study and practice at the parent company with high cost. This is actually a form of transfer pricing.

- MNCs branches hire consultants from the parent company and pay the cost, but it is difficult to determine the quantity and effectiveness, so it is difficult to assess whether the cost is high or low, appropriate or not fit. Although the tax authorities found that it was unusual, there was no basis to determine the act of price and cost overstatement to handle the business.

As a rule, the more you do business, the more you experience, the lower your costs, but the higher the management costs in these businesses. As a type of expense that is heavily related to the internal operation of the enterprise, based on internal regulations and contracts, this is also a cost that is very easy to raise, reduce profits or even causing losses, eroding tax bases, evading tax obligations. The exceptionally high salaries of senior employees from the parent company or from an organization with similar interests are also often the factor that pushes the input costs. It is worth mentioning that when FDI enterprises implement this form of transfer pricing, domestic joint venture partners are the ones who suffer most of their interests because it is impossible to determine the exact amount of costs to be spent compared to the with the benefits they get.

Transfer pricing through enhanced advertising costs

This is a transfer pricing method used by many multinational companies and FDI enterprises. This method is especially used if the FDI enterprise exists as a joint venture with the controlling capital of the foreign partner.

Raising advertising costs, especially in cases where the host country lacks strict regulations on determining reasonable advertising costs, the level of advertising, the ratio of advertising costs to total costs ... This method can help FDI enterprises achieve many goals: creating the phenomenon of virtual losses (revenue is very high but costs are higher); brand image dominates the market.

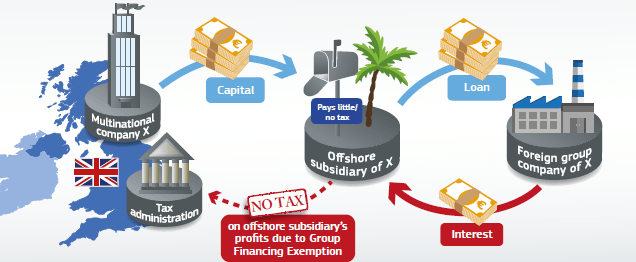

Transfer pricing through direct lending

One of the most popular forms today is the phenomenon of transfer pricing through loans between members in an MNCs. There are 2 cases where MNCs usually apply this transfer pricing method:

- When a profitable business branch in a country with a high corporate income tax rate, it will lend to the parent company or other affiliates at a low interest rate (even without interest) to help. All MNCs have capital to expand the market.

- When the branch is located in a country with a high CIT rate, they can borrow from the parent company or other branches at a very high interest rate, thereby making profits before tax (minus interest. ) negative, avoid paying corporate income tax. Lenders are often located in a place where the tax rate on interest is low, making the maximum amount of profits earned by MNCs.

Interest rate transfer #

This is a very sophisticated form of transfer pricing of FDI enterprises - branches of MNCs. Some of the methods commonly used by MNCs to transfer interest rates are:

Firstly, The most noticeable thing is that some FDI enterprises, after a short period of operation, apply for conversion into joint stock companies to be listed on the stock market. In the process of implementation, many businesses have incorrectly assessed the value of their assets, took advantage of the conversion to "capitalize the property", sold off shares, or even transferred all capital out of the country. receiving investment, both bringing profits to the parent company, and causing a disturbance in that national capital flow.

Monday, Some of them are members of corporations and would like to be listed on the stock market; Associated enterprises have carried out the transfer price to increase profits of enterprises that will be listed on the stock exchange. This will falsify the financial statements of the issuing company, causing the value of shares to increase when listed; creating price falsification of the issued shares, causing artificial imbalance in supply-demand in the stock market, causing market disturbances.

Tuesday, in the process of preparing for an enterprise to obtain the exclusive right to process and distribute certain goods or services in order to compete for market share of that type of goods or services, the associated parties may transfer revenue, profits for that business. This form also creates distortions in financial statements and in the market assessment of investors, creates unequal competition among enterprises, and oppresses small and medium enterprises.

Wednesday, In the condition that many countries actively attract capital from outside with the goal of fast and sustainable growth, the Governments of those countries have many preferential policies for investors in many industries, many sectors, or when investing in different areas, associated enterprises have transferred their revenue and profits from other sectors, industries and areas not entitled to incentives. to reduce tax payable, increase the profit of the affiliate group.

Risk of business when not implementing transfer pricing declaration #

Transfer pricing has 2 main risks, including the risk of compliance with documents and transfer pricing declarations; risk of accountability when tax authorities inspect.

Regarding the risk of compliance with documents and transfer pricing declaration: can be minimized if complying well, filing in accordance with regulations, declaring fully as required by law.

For the accountability risk when the tax authority inspects: it can be reduced if the enterprise actively researches the price transfer early, how to perform, how to identify associated parties, associated transactions, and determine the valuation, get to know the cost to be deducted when the price is transferred, the condition is deducted.

If you do not understand, do not comply well and know how to explain, the business may be subject to tax imposition, additional tax payable, arrears, tax penalties, late payment interest.

In addition, from the perspective of multinational companies, the impact of not declaring transfer prices leads to a decrease in the image and reputation of MNCs, even being affected by the governments of other countries where they have established subsidiaries. as well as the government of the country where it is headquartered investigates transfer pricing.

The tax authority has the power to set taxes when #

- Taxpayers fail to declare or provide insufficient information or submit Appendix 01 to the Decree on related transactions;

- Taxpayers provide incomplete information on transfer pricing documentation specified in Appendices 01 and 03 enclosed with the Decree on related transactions;

- Failure to present the associated transaction price determination dossier and other data, vouchers and documents used as a basis for analysis, comparison and price determination in the associated transaction price determination dossier at the request of Tax agencies within the time limit prescribed by the Decree;

- Taxpayers use information about untruthful or impractical independent transactions to analyze, compare, declare and determine the associated transaction price;

- Based on illegal, invalid documents and data;

- Do not specify the source of origin to determine the price, profit rate or profit distribution rate applicable to associated transactions;

- Taxpayers commit a violation of transfer pricing regulations in the transfer pricing Decree.