Recently, Deputy Prime Minister Le Minh Khai issued Decree 12 / 2023 / ND-CP come into force from the date 14.04.2023 until the end of the day 31.12.2023 on the extension of tax payment time and land rent in 2023, including value added tax (VAT), corporate income tax (CIT), personal income tax (PIT).

The content of extending the deadline for paying tax and land rent in 2023 is as follows:

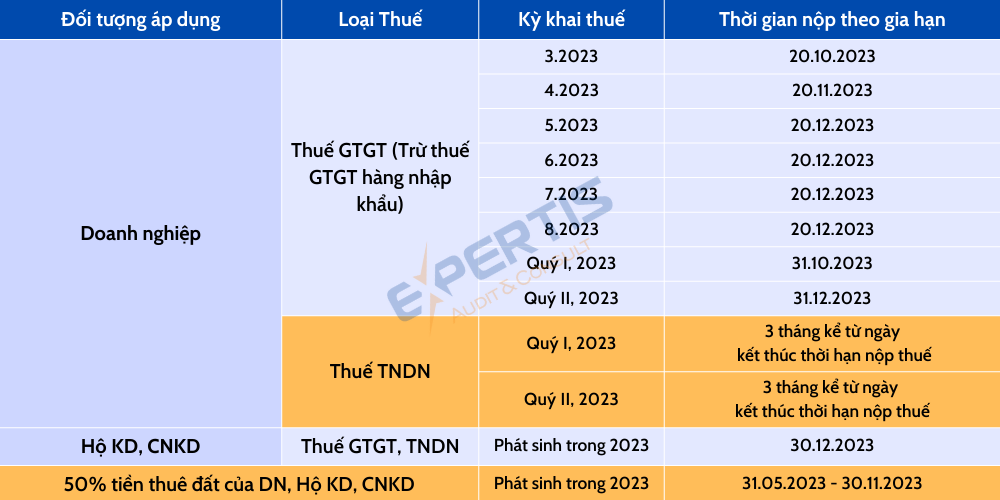

1. Extension of time limit for payment of VAT (except for import VAT)

Regulations on the extension of time for payment of VAT (except for VAT at the import stage) that must be paid (including tax distributed to other provinces and provinces where the taxpayer is headquartered, and the amount of tax to be paid each time). incurred) of the tax period from March to August 3 (in case of monthly declaration) and the tax period of the first quarter - II of 8 (in case of quarterly declaration) as follows:

VAT from March to May 3 and the first quarter of 5, the extension period is 2023 months;

- VAT of June 6 and the second quarter of 2023, the extension period is 2023 months;

- VAT of July 7, extension period is 2023 months;

- VAT of August 8, extension period is 2023 months.

Enterprises and organizations are entitled to an extension of time to declare and submit monthly and quarterly VAT declarations according to current regulations, but must NOT pay the payable VAT amount arising on the declared VAT declaration.

The extension period starts from the end of the time limit for VAT payment as prescribed by law. Specifically, the deadline for VAT payment upon extension is as follows:

- The tax period of March 3.2023 is extended the tax payment deadline to October 20.10.2023, XNUMX;

- The tax period of March 4.2023 is extended the tax payment deadline to October 20.11.2023, XNUMX;

- Tax period of May, June, August, 5,6,7,8, the deadline for tax payment will be extended to December 2023, 20.12.2023 at the latest;

- The tax period of the first quarter of 2023 is extended the tax payment deadline to October 31.10.2023, XNUMX at the latest;

- The tax period for the second quarter of 2023 is extended the tax payment deadline to December 31.12.2023, XNUMX.

In case branches and affiliated units make separate declaration of value added tax with the tax agency directly managing the branch or affiliated unit, the branches and affiliated units are also subject to tax exemption. VAT payment deadline.

In case a branch or affiliated unit of an enterprise or organization that is eligible for tax extension does not have production and business activities in the economic sector or field subject to the extension, the branch or affiliated unit is not eligible for tax extension. extension of payment of value added tax.

2. Extension of time for temporary payment of corporate income tax for the first and second quarters of 2023

The extension period is 3 months from the end of the CIT payment deadline as prescribed by law.

Branches, affiliated units of enterprises and organizations that are eligible for CIT payment extension when making separate CIT declarations with the tax authorities directly managing branches and affiliated units are also subject to CIT payment extension. icon is extended.

Branches and affiliated units of enterprises and organizations that do not have production and business activities in the economic sectors or fields that are extended are not eligible for the extension of CIT payment.

3. Extension of time for payment of VAT and personal income tax of business households and individuals

The tax payment time limit is extended to December 30.12.2023, XNUMX when business households and individuals operate in the economic sectors and fields specified in this Decree.

4. Land rent extension

The extension period is 06 months (from May 31.5.2023, 30.11.2023 to November XNUMX, XNUMX) for 50% the arising land rent payable in 2023 of enterprises, organizations, households, business households and individuals subject to regulations being directly leased land by the State.

Subjects eligible for extension of tax and land rent payment

According to this Decree the Subjects eligible for extension of VAT, PIT, CIT and land rent include the following 4 groups of subjects:

- Enterprises, organizations, households, business households and individuals engaged in production activities in the following economic sectors:

- Agriculture, forestry and fisheries;

- Manufacturing industries: apparel, leather and related products; products from straw, straw, plaiting materials; paper and paper products; products from rubber and plastics; other non-metallic mineral products; metal; manufacturing electronic products, computers and optical products; automobiles and other motor vehicles; beds, cabinets, tables, chairs; mechanical; metal treatment and coating; food production and processing; weaving; wood processing and production of products from wood, bamboo and cork (except for beds, cabinets, tables and chairs);

- Build;

- Publishing activities; cinematography, television program production, sound recording and music publishing;

- Exploiting crude oil and natural gas

- Beverage production; print, copy records of all kinds; production of coke, refined petroleum products; manufacture of chemicals and chemical products; manufacture of products from prefabricated metal (except for machinery and equipment); manufacture of motorcycles and motorbikes; repair, maintenance and installation of machinery and equipment;

- Drainage and wastewater treatment.

- Enterprises, organizations, households, business households and individuals conducting business in the following economic sectors:

- Warehouse transportation; accommodation and catering services; educations; health care, social assistance; real estate;

- Labor and employment services; travel agency, tour business and support services;

- Creative, arts and entertainment; libraries, archives, museums and other cultural activities; sports, entertainment; movies;

- Broadcasting; programming, consulting and other computer-related activities; information services;

- Mining support services.

- Enterprises, organizations, households, business households and individuals engaged in production of supporting industry products are prioritized for development; key mechanical products.

- Small and micro enterprises are defined in accordance with the Law on Supporting Small and Medium Enterprises 2017.

Taxpayers eligible for extension of time limit for paying tax and land rent Application letter for extension to the tax authority directly managed before the date 30 month 9 year 2023 to be extended as specified.